First Quarter 2026 Quarterly Market Recap

The U.S. labor market spent 1Q26 in what the Stanford Institute for Economic Policy Research described as a “low-hire, low-fire equilibrium”. Layoffs remained historically low, and the unemployment rate held near the full-employment level economists generally associate with the natural rate (i.e., around 4.0% to 4.1%). However, gross hiring activity remained subdued, and payroll growth was narrowly concentrated in just a few sectors, leaving the headline numbers more fragile than their surface stability suggested.

The U.S. economy entered 2026 with sustained momentum, as Real GDP grew at a 4.4% annualized rate in Q3 2025 and an estimated 2.0% in 4Q25. The 4Q25 slowdown partly attributable to the government shutdown that disrupted federal activity in October. Full-year 2025 growth came in at approximately 2.0%, consistent with or slightly above long-run trend, a notably solid result given the cumulative headwinds from elevated interest rates and policy uncertainty. Business investment was another constructive driver of GDP growth, as AI-related capital expenditures accounted for a disproportionate share of non-residential investment in 2025. However, the return on investment (ROI) debate around these outlays has generated ongoing scrutiny from investors.

Outlook

Despite the volatility seen during the first quarter, the underlying U.S. economy remains on reasonably solid footing. Consumer spending has held up, GDP growth is tracking near potential, and the broader economic expansion shows few signs of rolling over. The resilience is notable given the cumulative weight of elevated interest rates and geopolitical uncertainty.

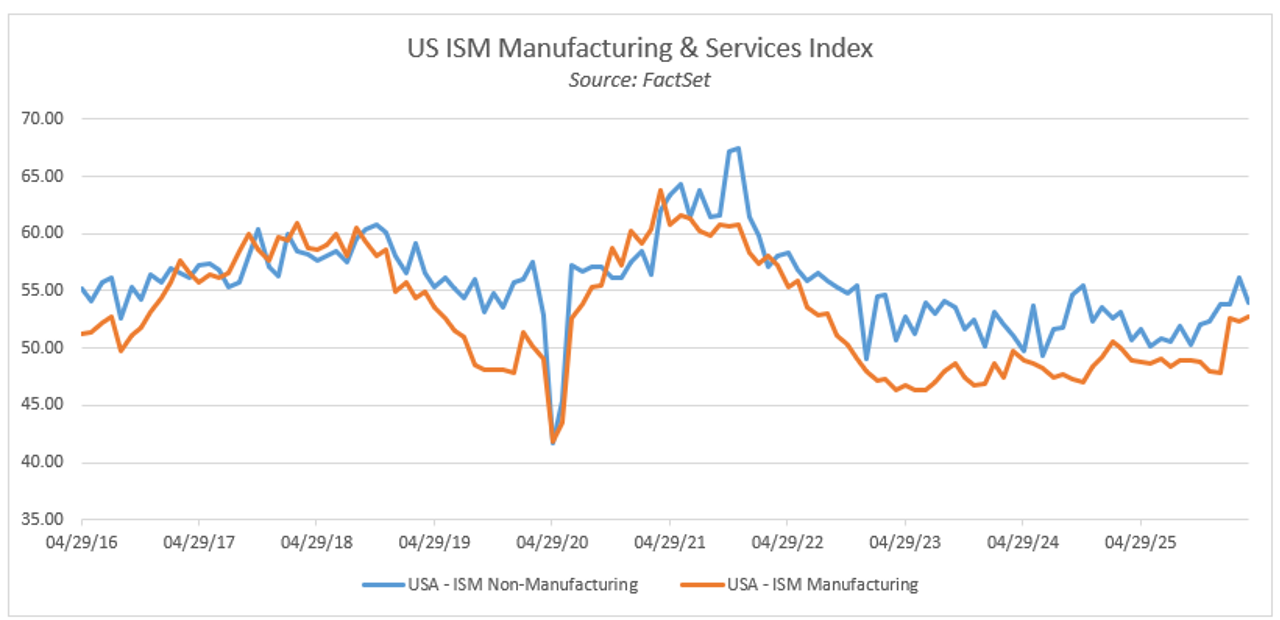

One encouraging development is the nascent recovery in the manufacturing sector. The US ISM Manufacturing Index has now inflected positively for three consecutive months. This is a streak that has historically signaled a broadening of economic activity beyond the consumer and services sectors. The labor market, while cooling at the margin, remains stable. Layoffs are not elevated, the unemployment rate is holding near full-employment levels, and wage growth continues to support household purchasing power. The hiring environment is cautious, but there is little in the current data to suggest a material deterioration is imminent.

Taken together, the economic backdrop for the remainder of 2026 is more constructive than recent market volatility might imply. The primary risk remains the duration and resolution of the Iran conflict and its inflationary effects. However, absent a significant further escalation, the foundation for a continued, modest expansion for the US economy appears intact. At Oliver Luxxe, our "Private Equity in the Public Marketplace" investment philosophy is driven by identifying businesses with durable balance sheets, consistent cash flow generation, and attractive opportunities to reinvest capital for long-term growth. Across our equity strategies, we view market volatility as an opportunity rather than a risk. Periods of uncertainty allow us to upgrade portfolio quality and add to high-conviction positions at more attractive valuations.

As always, please feel free to reach out to us if you have any questions. Thank you.