White Paper: The GICS Industrials Sector

The GICS Industrials Sector: Structure, Scope, and Opportunity Set

Executive Summary

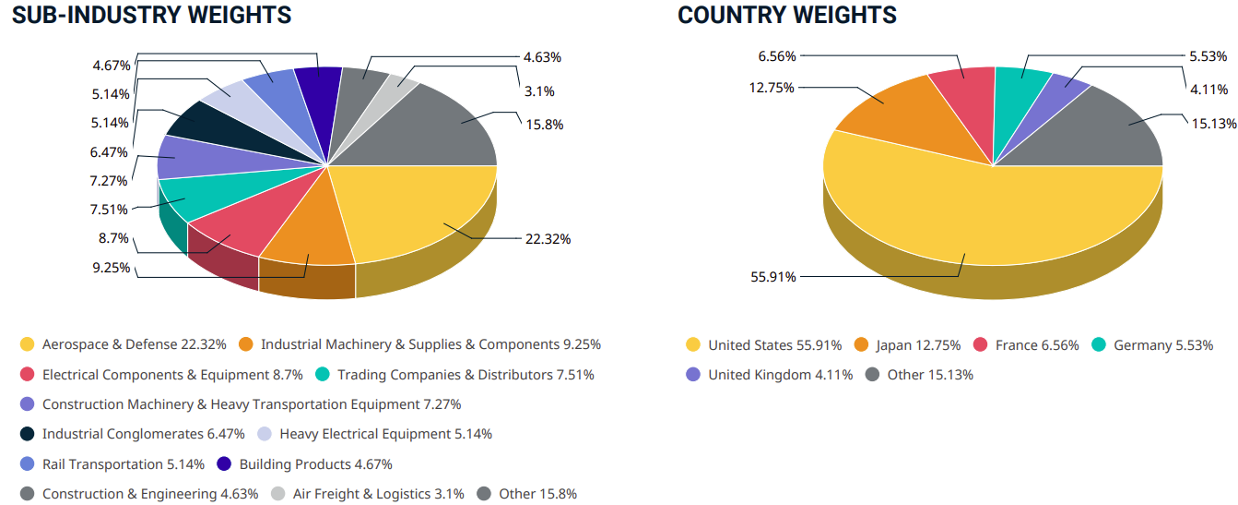

The Industrials sector, as defined by the Global Industry Classification Standard (GICS), represents one of the broadest and most diversified opportunity sets available to equity investors. The MSCI World Industrials Index captures 257 large- and mid-cap constituents across 23 developed market countries, representing approximately $9.4tn in total market capitalization as of March 31, 2026. The Industrials sector spans 3 industry groups, 14 industries, and >20 sub-industries. This white paper provides an overview of the Industrials sector using the MSCI World Industrials Index as the primary lens, along with the Global Industry Classification Standard (GICS).Sub-Industry Composition

The three GICS Industrial industry groups include 1.) Capital Goods (Aerospace & Defense, Building Products, Construction & Engineering, Electrical Equipment, Industrial Conglomerates, Machinery, Trading & Distributors), 2.) Professional Services (Commercial Services & Supplies and Professional Services), and 3.) Transportation (Air Freight & Logistics, Airlines, Marine, Road & Rail, and Transportation Infrastructure). The breadth of the sector is evident in its sub-industry composition. Aerospace & Defense is the largest sub-industry, representing 22.32% of the index. However, no other single sub-industry exceeds 10%, and the bottom tier (i.e., "Other") collectively accounts for 15.80%.

Source: MSCI World Industrials Index

Benchmark Weightings as of 3/31/26

The Industrials sector commands meaningful weight across the two most widely used value benchmarks in the United States. At 16.02% of the Russell 1000 Value Index and 12.40% of the Russell 2000 Value Index, Industrials represents one of the largest sector allocations that active value managers must contend with. For managers benchmarked to either index, the sector's breadth across sub-industries means that stock selection within Industrials can be a significant source of alpha generation. Whether an active manager is overweight Aerospace & Defense names at the large-cap level or finding mispriced small-cap Machinery companies, the depth of the sectors’ opportunity set offers a wide canvas for differentiated positioning relative to the benchmark.

Cyclical vs Secular

The Industrials sector has historically been viewed as a collection of largely cyclical end markets, with less secular-driven growth compared to other GICS sectors. The cyclicality of the sector comprises most of the sub-industries, but the growing divergence in end-market drivers across those sub-industries means that not all Industrials names will move in lockstep with the economic cycle, creating meaningful opportunities for active managers to differentiate. Several secular themes are driving sustained demand across the sector's sub-industries, including the buildout of datacenter and AI infrastructure, the reindustrialization and reshoring of domestic manufacturing capacity, the adoption of automation and robotics across production environments, and the expansion and modernization of power generation assets to meet rising electrification needs.

The convergence of these structural tailwinds with the sector's inherent cyclicality means that Industrials can offer investors both a way to participate in economic recoveries and a vehicle for accessing multi-year capital investment cycles that may be less sensitive to short-term GDP fluctuations than the sector's historical reputation would suggest.

Calculating Mid-Cycle Earnings

For cyclical Industrials companies, revenue and margins can swing meaningfully, which makes establishing a credible estimate of mid-cycle earnings power essential. This requires rigorous bottom-up fundamental analysis through a detailed examination of a company's revenue composition, its historical margin behavior across prior cycles, and the sustainability of operational or pricing improvements that may have structurally shifted the business's normalized earnings trajectory (see our 80/20 white paper here). Without this level of due diligence, investors risk overpaying for businesses that appear inexpensive on peak earnings, or dismissing under-earning businesses at trough multiples (i.e., artificially high).

Conclusion

The Industrials sector is one of the most expansive and varied corners of the global equity market, offering investors access to a diverse set of end markets. The sector ranges from Aerospace & Defense to Professional Consulting industries. Its considerable weight in both the Russell 1000 Value and Russell 2000 Value Indices makes it a sector that active managers cannot afford to overlook, as even modest over- or underweights can materially impact relative performance.

What makes the current environment particularly interesting is that the sector is no longer defined solely by its sensitivity to the economic cycle. A new generation of capital investment themes around electrification, AI-related infrastructure, and supply chain localization is creating pockets of demand that may persist independent of GDP growth. That said, much of the sector remains tied to cyclical dynamics, which means the ability to distinguish between companies benefiting from structural change and those simply riding a cyclical upswing is critical. Getting that distinction right ultimately comes down to fundamental research. For example, understanding where a business sits in its earnings cycle, what a normalized level of profitability looks like, and whether recent margin gains reflect lasting operational improvement or temporary tailwinds remains of high importance.

At Oliver Luxxe Assets, our approach to investing is grounded in deep, bottom-up fundamental research, where we seek to identify high-quality businesses that offer a compelling combination of durable growth and reasonable valuations. Central to our process and discipline is a focus on return on invested capital (see our ROIC white paper here), which we view as an indicator of a management team's ability to allocate capital effectively and create long-term shareholder value. We favor companies that maintain clean, conservatively managed balance sheets that provide financial flexibility to invest through cycles and resilience during periods of economic uncertainty. Equally important is the quality of a company's reinvestment runway. We look for businesses with identifiable and attractive opportunities to deploy capital back into the business at returns that exceed their weighted average cost of capital, whether through organic growth initiatives, capacity expansion, or disciplined acquisitions.

Prepared by:

Drew R. Crawford Jr.

Director of Equity Research & Senior Research Analyst

Disclosures: This document contains forward-looking statements relating to the opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as “believe,” “should,” “planned,” “potential” and other similar terms. Examples of forward-looking statements include results of operations and success or lack of success of any particular investment strategy. All are subject to various factors, including, the general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals, nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

Disclaimer:

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction. All investment strategies have the potential for profit or loss; changes in investment strategies may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the US market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to the success or lack of success of any particular investment strategy. All are subject to various factors, including, to general and local economic conditions, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.